Imagine building a compliance report for your fintech app in one day instead of a week. No need to wait for engineers. No long sprint cycles. Just type what you need-like "Create a dashboard that flags suspicious transactions and auto-generates SOC 2 audit logs"-and the system builds it. That’s vibe coding in action.

What Is Vibe Coding, Really?

Vibe coding isn’t just another AI code assistant. It’s a shift from writing code to describing what you want. Coined by AI researcher Andrej Karpathy in early 2025, it uses large language models to turn natural language into working software. You don’t need to know Python, SQL, or JavaScript. You just need to be clear about your goal. In fintech, this matters because teams are drowning in complexity. Regulatory rules change. Data flows through dozens of systems. Engineers are stretched thin. Vibe coding lets product managers, risk analysts, and operations staff build tools themselves-without waiting for a dev team. Platforms like Superblocks, Replit, and Cursor have turned vibe coding from a novelty into something enterprises actually use. These aren’t just autocomplete tools like GitHub Copilot. They’re agentic systems. They can run for hours, connect to APIs, generate mock data, test outputs, and even loop back to refine their own work-all guided by your initial prompt.Why Mock Data Is the Secret Weapon

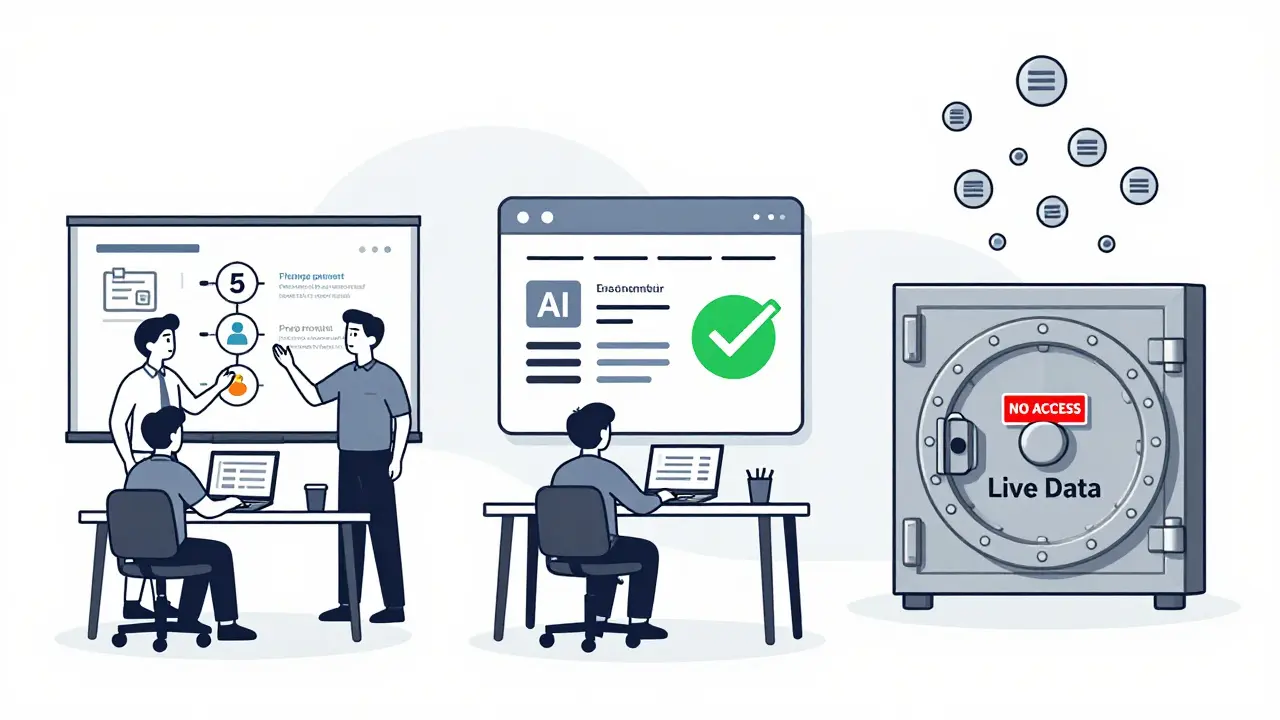

You can’t test a fraud detection tool with real customer data. That’s illegal. You can’t use live bank feeds during development. Too risky. So you need mock data-fake but realistic transaction patterns, user profiles, KYC documents, and payment histories. Vibe coding platforms now auto-generate this data. You say: "Generate 10,000 synthetic transactions with 3% fraud rate, including ACH reversals, cross-border payments, and duplicate merchant IDs." The system builds it. It doesn’t just copy-paste random numbers. It understands financial behavior. It mimics how real users behave-spikes on payday, small test transactions before large ones, unusual login times. A UK fintech startup in 2025 used this to cut their fraud model testing time from 3 weeks to 4 days. They didn’t need to hire data engineers. They didn’t need to scrub real data. The AI created datasets that passed both technical and compliance checks. But here’s the catch: bad mock data gives you false confidence. If the AI generates transactions that are too clean, your system won’t catch real fraud. If it doesn’t include edge cases-like partial refunds, currency conversions, or holiday spikes-you’ll get burned in production. The best teams don’t just ask for data. They specify constraints: "Include 5% of transactions with mismatched billing addresses but valid CVV. Simulate 2% of users with expired IDs. Add 100 cases where the IP location doesn’t match the card’s country." That level of detail turns mock data from a placeholder into a training ground.Compliance Isn’t Optional-It’s Built In

Fintech isn’t like a mobile app for cat memes. One mistake can mean fines, lawsuits, or jail time. That’s why vibe coding in finance doesn’t just build apps-it builds guardrails. Enterprise platforms now embed compliance rules directly into the AI’s output. When you prompt for a customer onboarding tool, the system doesn’t just generate a form. It automatically adds:- Role-based access control (RBAC) so only authorized staff see sensitive data

- Audit trails that log every change, who made it, and when

- Encryption at rest and in transit

- GDPR and SOC 2 compliance checks baked into the code

Guardrails: The Invisible Safety Net

Vibe coding gives you speed. But speed without control is chaos. That’s why guardrails are non-negotiable. These aren’t firewalls or passwords. They’re behavioral rules the AI follows automatically:- No direct access to live payment systems unless explicitly approved

- Automatic redaction of PII (personally identifiable information) in logs

- Blocking code that uses deprecated or vulnerable libraries

- Requiring human approval before deploying to production

Who’s Using This-and Who Isn’t?

By Q2 2025, 37% of fintech startups were using vibe coding for at least one internal tool. Traditional banks? Only 22%. Why the gap? Startups move fast. They don’t have legacy systems. They don’t have compliance teams buried under 100-page policies. They’re building tools to test ideas-like a new onboarding flow or a real-time liquidity tracker. Vibe coding lets them prove value before hiring engineers. Banks? They’re cautious. Their systems run on COBOL and mainframes. Their regulators demand paper trails. Their legal teams still print out every change request. So they’re starting small: internal dashboards, reporting tools, employee onboarding checklists. Nothing customer-facing. Not yet. The tools being built? Three main categories:- 63%: Compliance and audit reporting

- 58%: Internal operational tools (HR, finance, IT)

- 42%: Fraud monitoring and anomaly detection

The Learning Curve: It’s Not About Coding

You don’t need to be a developer to use vibe coding. You need to be clear. The biggest hurdle? Writing good prompts. Most failures happen because people type vague stuff like: "Make a tool for fraud." That’s not enough. Successful teams train their non-technical staff to think like this:- What’s the goal? (e.g., detect fake accounts)

- What data do I need? (e.g., email, phone, IP, device fingerprint)

- What’s the threshold? (e.g., flag if 2+ factors are inconsistent)

- What’s the action? (e.g., block sign-up, send alert to analyst)

- What’s the compliance rule? (e.g., GDPR requires consent logging)

The Future: AI That Knows the Rules

The next leap isn’t faster code. It’s smarter compliance. Superblocks announced in December 2025 that they’re building AI-powered compliance validation. Imagine this: you write a prompt. The AI generates code. Then it automatically checks that code against every active regulation in your jurisdiction-real-time, from official government databases. No manual review. No spreadsheets. Just a green light or a highlighted violation. Gartner predicts that by 2027, 60% of internal fintech tools will be built with vibe coding. But core systems? Still human-coded. Why? Because regulators aren’t ready to trust AI with money movement. Not yet. The real winners won’t be the ones who build the fastest. They’ll be the ones who build the most trustworthy. That means pairing speed with structure. Innovation with oversight. As Riccardo Balsamo of Tenity put it: "Innovation without governance is just improvisation." Vibe coding doesn’t remove the need for rules. It makes them easier to follow.What You Should Do Next

If you’re in fintech and wondering where to start:- Find a small, low-risk tool to automate-like a weekly report or internal checklist.

- Choose a platform with built-in compliance guardrails (Superblocks, Replit Enterprise).

- Work with your compliance team to write the first prompt together.

- Use synthetic data. Never use real customer data in development.

- Run a weekly audit. Check for drift.

- Don’t try to replace your core systems. Start with the boring stuff.

Frequently Asked Questions

Can vibe coding replace software engineers in fintech?

No. Vibe coding shifts their role. Engineers still design systems, set guardrails, audit outputs, and handle complex logic that AI can’t manage-like real-time payment routing or fraud pattern detection at scale. They’re no longer writing every line of code, but they’re still the ones ensuring safety, reliability, and scalability.

Is vibe coding secure for financial data?

Only if the platform is built for finance. Enterprise-grade vibe coding tools use encrypted data pipelines, role-based access, and audit trails. They don’t store real customer data-they use synthetic mock data. Always verify that the platform is SOC 2 certified and complies with your jurisdiction’s data laws before using it.

What’s the biggest mistake teams make with vibe coding?

Assuming the AI gets compliance right on the first try. Most teams fail because they treat it like a magic box. Vibe coding requires collaboration. Compliance officers must help write prompts. Developers must review outputs. Regular audits are non-negotiable. Speed without oversight leads to regulatory risk.

Can I use vibe coding for customer-facing apps?

Not yet for most regulated institutions. Current tools are best for internal tools-reporting, dashboards, workflows. Customer-facing apps require real-time performance, zero tolerance for errors, and full auditability. While some startups are experimenting, enterprise banks are holding off until regulators give clear guidance. Start with internal tools first.

How do I know if my vibe-coded tool is compliant?

Run a compliance checklist against it. Does it log all user actions? Does it encrypt data? Does it restrict access properly? Does it meet GDPR, SOC 2, or PCI DSS requirements? Use automated validation tools built into platforms like Superblocks. If your tool doesn’t pass a manual audit by your compliance team, it’s not ready for production.

Artificial Intelligence

Artificial Intelligence

Kelley Nelson

January 23, 2026 AT 16:03While the notion of 'vibe coding' is undeniably fashionable, one must question whether its adoption in regulated environments constitutes a superficial veneer over deeply entrenched systemic risks. The presumption that natural language prompts can reliably encode compliance logic ignores the ontological complexity of financial regulation - a domain governed not by semantics, but by jurisprudential nuance, precedent, and institutional inertia. To conflate prompt engineering with governance is to mistake syntax for substance.

Aryan Gupta

January 23, 2026 AT 21:50lol so now ai is gonna write our compliance docs? next they'll be signing off on auditors' signatures with a 'vibe check'. fake transactions? yeah right. this is just a backdoor for data leaks. i bet these 'enterprise platforms' are all hosted on aws and feeding data to china. you think they care about soc2? they care about vc funding. they'll sell your customer data before the first audit. watch. this is how they get you hooked. then one day your bank gets hacked and the ai 'forgot' to log the consent timestamps. classic.

Fredda Freyer

January 25, 2026 AT 01:02There’s something profoundly human about this shift - not in the code, but in the redefinition of who gets to build. For years, compliance was a gatekept domain, reserved for those who spoke the dialects of Java, SQL, and regulatory legalese. Vibe coding doesn’t erase expertise; it redistributes agency. A risk analyst who understands fraud patterns better than any junior dev can now prototype a detection engine without waiting for sprint planning. The real innovation isn’t the AI - it’s the collapse of the hierarchy between domain knowledge and technical execution. That said, the danger lies in mistaking speed for wisdom. The best tools don’t just generate code; they generate conversation. The prompt becomes a ritual: a shared space where compliance officers, engineers, and operators negotiate meaning - not through tickets, but through language. That’s the quiet revolution.

Gareth Hobbs

January 26, 2026 AT 09:21oh great. another american tech bro fantasy. we in the uk have been dealing with real compliance for decades - not this 'vibe' nonsense. you think a prompt can handle fca rules? lol. they'll let you build a tool that auto-generates a report and then slap you with a £200m fine because it missed a comma in a footnote. and dont get me started on the 'mock data' - you think some ai knows how a brit pays their utility bill? it'll generate 10k transactions with 'london' as the ip and 'cardiff' as the billing address and call it 'realistic'. absolute farce. and now you want us to trust this with our banking? i'd rather use pen and paper. #britishcommonsense #aiisarisk

Zelda Breach

January 28, 2026 AT 06:13Let me guess - the next thing you'll say is that a 16-year-old intern with a ChatGPT Plus subscription can now replace your entire compliance department. How quaint. You didn't mention the 17 lawsuits already filed against companies using 'vibe-coded' audit trails that didn't log user consent timestamps because the AI 'assumed' implied consent. The only thing faster than the code generation is the rate at which these tools are getting flagged by regulators. Spoiler: compliance isn't a prompt. It's a liability. And you're handing it to a language model trained on Reddit threads.

Alan Crierie

January 29, 2026 AT 17:22Really appreciate this breakdown - it’s rare to see someone articulate the balance between speed and safety so clearly. I’ve seen teams try vibe coding and just throw out the guardrails because ‘it works’. But as you said, it’s not about replacing engineers - it’s about redefining their role. I’ve started using Superblocks for internal HR onboarding checklists, and the compliance team actually asked to join the prompt-writing sessions. It’s become this weirdly collaborative ritual. We even built a little emoji badge system: 🟢 for compliant, 🔴 for drift, 🟡 for ‘needs a human to squint at this’. It’s silly, but it works. Keep the human in the loop. Not as a gatekeeper - as a co-creator. 🙌